Quantitative Easing (QE) Explained: Central Bank Tool for Growth (Part 1)

QUANTITATIVE EASING EXPLAINED: MAIN TALKING POINTS

- With interest rates near zero, the Federal Reserve ventured another policy tool in quantitative easing

- After years of QE, the Bank of Japan has experienced diminishing economic and financial returns

- Similarly, the ECB has engaged in long-term refinancing operations (LTROs) as a form of quantitative easing, but their effectiveness remains in question

HOW DOES QUANTITATIVE EASING WORK?

Pipscollector.com - Quantitative easing (referred to as ‘QE’) is a monetary policy tool typically used by central banks to stimulate their domestic economy when more traditional methods are spent. The central bank buys securities – most frequently government bonds – from its member banks, effectively increasing the supply of money in the economy.

With increased supply, the cost of money is reduced which makes it cheaper for businesses to borrow money to use for expansion. This has a similar effect to the standard interest short-term interest rate cuts that central banks employ; but depending on what they purchase, such efforts can lower the cost for significantly longer loans. That could more directly influence lending for homes, autos and small businesses.

THE FEDERAL RESERVE BANK (FED) QUANTITATIVE EASING POLICY

As the central bank of the United States, the Federal Reserve has a duty to provide the nation with a safer, flexible and more stable monetary and financial system. That is often boiled down into a stated dual mandate of steady inflation and low unemployment. In pursuit of these objectives, the Fed is allotted a series of monetary policy tools that allow it to influence the US Dollar and the money supply in the country. While raising and lowering the Federal Funds rate is the most widely known tool, the central bank’s balance sheet has become one of heightened importance and investor interest.

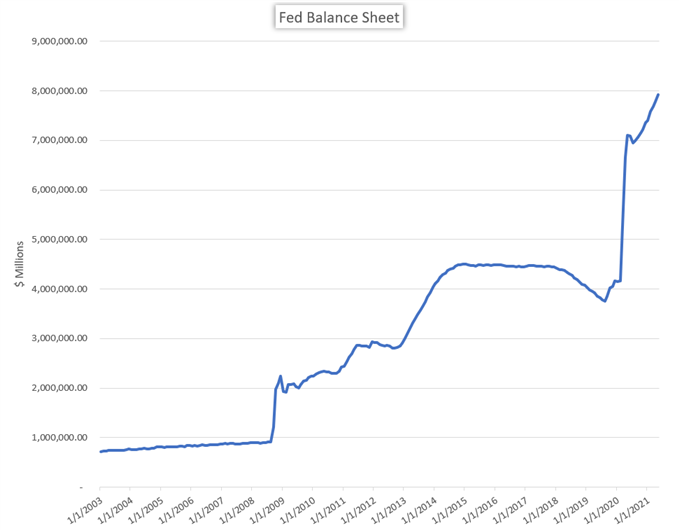

FEDERAL RESERVE BANK TOTAL ASSETS

Source: FRED

Simply put, the Fed’s balance sheet is the same as any other balance sheet. In the Fed’s case, it records the collection of distinct assets and liabilities across all the Federal Reserve bank branches. The bank can use these assets and liabilities as an unconventional or supplementary monetary policy tool, particularly when interest rates are already low and confer limited potential with further policy efforts.

In 2008, as the United States economy entered a recession amid the Great Financial Crisis, the Federal Reserve announced a series of interest rate cuts. As a typical expansionary tool, the cuts were intended to spur spending thereby improving the economy. However, even with interest rates near zero, economic recovery failed to take hold.

Then, in November 2008, the Federal Reserve announced its initial round of Quantitative Easing, popularly known as QE1. The announcement saw the Fed massively shift its standard market operations as it began to purchase significant amounts of treasury bills, notes and bonds, along with asset- and mortgage-backed securities of high quality. The purchases effectively increased the supply of money in the US economy and made access to capital less expensive. The buying program lasted from December 2008 to March 2010 and was accompanied by another cut to the Fed Funds rate, resulting in a new range of 0 to 0.25% interest.

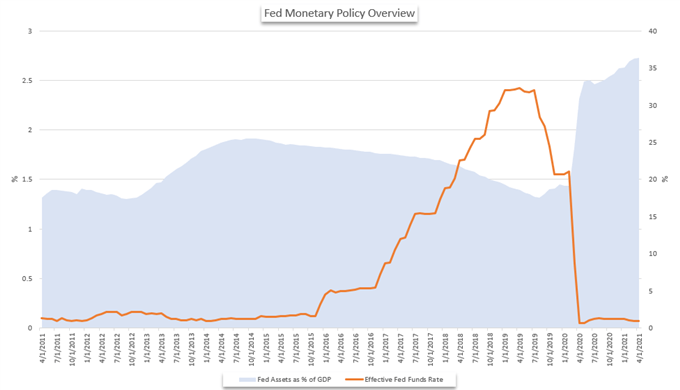

CHANGE IN FED BALANCE SHEET DUE TO QUANTITATIVE EASING

Source: Bloomberg

With the Federal Funds rate near 0, and not willing to explore negative rates at the time, the central bank had effectively expended all its expansionary monetary policy tools. Thus, quantitative easing became an important part of the central bank’s toolbox to boost economic growth and right the capsized ship that was the US economy.

To further aid recovery, the Fed pursued subsequent rounds of Quantitative Easing, now known as QE2 from November 2010 to June 2011 and QE3 from September 2012 to December 2013. The purchase programs targeted similar assets and helped to prop up perceived growth – as well as capital markets as a side effect – in the US until the central bank finally reversed course by raising its benchmark rate for the first time in December 2015.

Having already started to reduce its balance sheet in 2018, we have seen debate over a sustained Quantitative Tightening (reducing the balance sheet) pop up in 2019. Many Federal Reserve officials have supported the slow drawdown of the bank’s balance sheet and advocated for further normalization as the US economy boasts over a decade of economic expansion. However, uneven growth and external risks like trade wars have complicated the issue of this exceptional support.

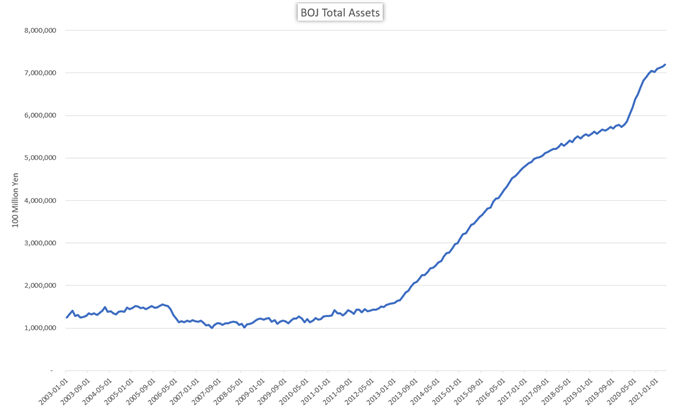

THE BANK OF JAPAN (BOJ) QUANTITATIVE EASING POLICY

Japan’s central bank is another financial institution that has employed the use of quantitative easing, but with varying degrees of success. One of the first instances occurred between October 1997 and October 1998 when the BOJ purchased trillions in Yen of commercial paper in an attempt to help banks through a period of low growth, low interest rates and trouble from bad bank loans. However, growth remained subdued.

View our Economic Calendar for data releases and live event times.

In light of the underwhelming impact, the Bank of Japan increased asset purchases between March 2001 and December 2004. This round of purchases targeted long-term government bonds and injected 35.5 trillion Yen in liquidity to Japanese banks. While the purchases were moderately effective, the purchase of long-term government bonds suppressed asset yields and at the advent of the Great Financial Crisis, Japan’s growth vanished once again. Since then, the Bank of Japan has conducted numerous rounds of QE and qualitative monetary easing (QQE) all of which were largely ineffective as the country struggles with low economic growth despite a negative interest rate environment.

Source: Bloomberg

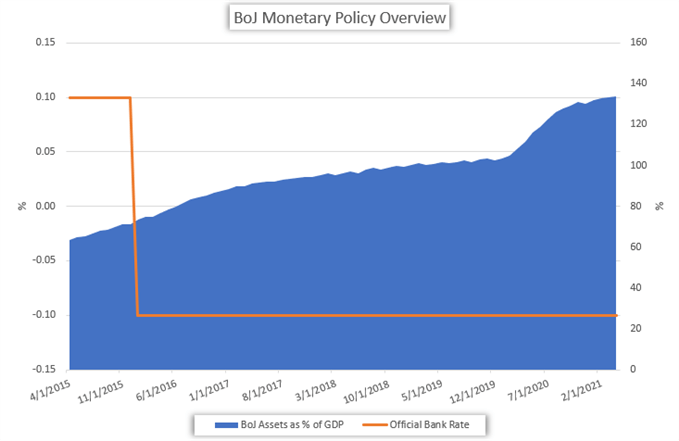

Today, the Bank of Japan has branched out to other forms of asset purchases with varying degrees of quality. Alongside previous purchases of commercial paper, the bank has built up considerable ownership of the country’s exchange traded fund (ETF) market and Japanese real estate investment trusts or J-REITs.

Source: Bloomberg

The BOJ began ETF purchases in 2010 and as of 2Q 2018 owned roughly 70% of the total Japanese ETF market. Further, these broad purchases have made the central bank a majority shareholder in over 40% of all public Japanese corporations according to Bloomberg. Thus, the quality and credit rating of these holdings by the central bank are fundamentally weaker than that of a government issued assets like Japanese Government Bonds (JGBs) and differ considerably from holdings of the Federal Reserve.

Read more articles in the Educational Content category to update the latest forex knowledge from Pipscollector.

- Pipscollector -