Central Banks and Monetary Policy: How Central Bankers Set Policy (Part 2)

CONVENTIONAL V/S UNCONVENTIONAL POLICY TOOLS

Pipscollector.com - Before the financial crisis, the toolkit of most central banks was relatively standard. These central banks would set a short-term interest rate and control bank lending through reserve requirements and other similar metrics. The major exception to these simple operating tools was the Bank of Japan, which began to embark on “unconventional” policy tools beginning in the late 1990s, as Japan struggled to escape a major recession and deflation.

In the aftermath of the financial crisis, economies around the world remained stuck in a state of shock. Global central banks, led by the Federal Reserve, began to adopt the same unconventional policies introduced by the Bank of Japan.

They purchased large amounts of government bonds to flood the financial system with liquidity and dropped and held their policy rates at zero or even in negative territory. During the crisis, central banks also used their lending powers to create new, targeted tools that could provide support to key areas of the financial system, like money market funds and large broker-dealers, that fell outside of the purview of traditional central bank support tools.

These unconventional tools have become a major part of the central bank’s toolkit and have been put to use to great effect during the Covid crisis. Beyond slashing policy rates back to the zero-lower bound, central banks expanded the scope of their support measures beyond anything seen during the financial crisis, pledging support to corporate bond markets, backstopping key areas of the financial system, and purchasing trillions in government bonds.

QUANTITATIVE EASING

Following the financial crisis, central banks set out on a journey to manipulate longer-term rates and flood the financial system with liquidity in order to better support economic spending, growth, and inflation. Through large-scale asset purchase programs, better known as quantitative easing (QE), central banks have bought large quantities of government debt from the open market.

Technically, these operations are similar to the traditional open market operations undertaken by central banks pre-crisis, just on a much larger scale. While the exact mechanism of action surrounding QE remains a point of debate, such programs drive down longer-term interest rates, help to support inflation, and oftentimes provide a tailwind to other financial markets.

QE has also risen in importance given the prolonged period of low rates that advanced economies have been faced with. Since central banks can no longer simply cut rates to the necessary level needed to jumpstart the economy during a recession, they have instead turned to further QE programs.

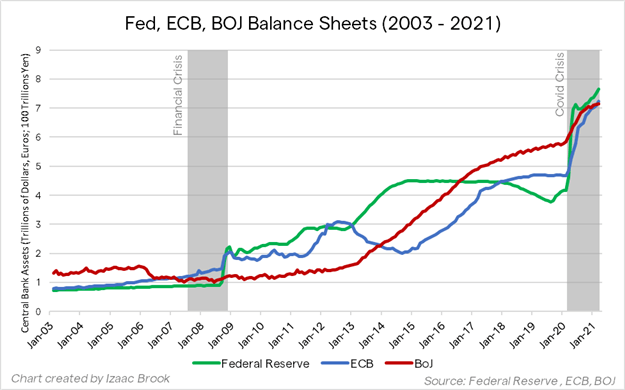

Research suggests that an asset purchase program equivalent to around 1.5% of GDP has a similar impact as 25 basis point interest rate cut. With US interest rates at only 1.50% before the Covid crisis, and rates elsewhere even lower, continued QE programs should supplement the deficiency in traditional rate cuts. As such, asset purchase programs have ballooned since the Covid crisis began, sending central bank balance sheets to record levels.

IMPLEMENTATION

These unconventional support measures are carried out by the central bank’s monetary policy implementation division. The implementation division is where central bank policy is actually put into effect through trading and technical adjustments made in financial markets. Policy decisions from head central bankers are passed to central bank traders, who then trade with specific counterparties to move rates or otherwise carry out policy decisions.

RATES SETTING: PRE-CRISIS

For the Federal Reserve, monetary policy is implemented through the Federal Reserve Bank of New York. Before the financial crisis, a decision on the Federal Funds Rate would be passed to markets desk traders. These traders would conduct open market operations with primary dealers.

Primary dealers are large banks approved as trading counterparties of the NY Fed, and are required to make markets and support the issuance of US Government debt (Treasuries). The NY Fed markets desk would buy or sell a certain amount of Treasuries from these banks, adjusting the supply of liquidity in the financial system and pushing short-term rates into the FOMC’s desired range.

This fine-tuning of liquidity was the process used by central banks around the world before the unconventional tools of the financial crisis were put to use. Once global financial systems were flooded with liquidity, policy setting had to evolve beyond this rudimentary method.

RATES SETTING: POST-CRISIS

Following the QE operations undertaken by central banks during the financial crisis, traditional open market operations would not have enough of an impact on liquidity and credit conditions to materially tighten or loosen interest rates. The Fed’s main policy lever became interest on reserves, the rate at which banks earn for storing “freshly-printed” QE money directly at the Fed.

Activity in the Federal Funds Market shrunk drastically as banks no longer needed to seek out funds to maintain regulatory requirements and also no longer desired to lend to other banks on an unsecured basis. Instead, interbank lending migrated to the repo market, where lending is secured against collateral.

The NY Fed’s repo and reverse repo facilities have become important tools for managing the excess liquidity in the system and the rates on these facilities are often adjusted alongside the Fed’s main policy rate.

The repo (RP) facility allows the Fed to lend to cash-seeking market participants against Treasury collateral, setting an upper-bound on interest rates.

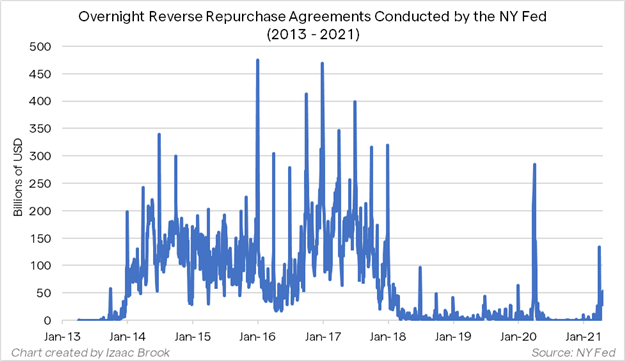

The reverse repo facility (RRP) is the opposite, where the Fed lends Treasury collateral to market participants with excess cash. The RRP facility serves as a temporary drain of reserves from the system and sets a lower-bound on interest rates.

During 2014 to 2018, the pre-Covid peak of the Federal Reserve’s balance sheet, the RRP facility saw huge uptake at quarter-end periods as excess cash was drained from elsewhere in the financial system, preventing rates from below the FOMC’s lower-end target.

With bank reserves at new record highs in the post-Covid environment, one should expect to see similarly-large usage of the RRP facility at future quarter-ends. The NY Fed raised the counterparty limit for the facility at the March 2021 FOMC meeting in preparation of future usage.

Read more articles in the Educational content category to stay up to date with the latest forex knowledge from Pipscollector.

- Pipscollector -